In questionnaires for the Flood insurance line, you might encounter the terms

Here's how to identify these for the property you want to insure.

CBRA area

The Coastal Barrier Resources Act (CBRA) of 1982 prohibits Federal funding for building and development in undeveloped portions of designated coastal barriers, including the Great Lakes and otherwise protected areas (OPAs).

These areas were mapped and designated as Coastal Barrier Resources System (CBRS) units. They are also called Coastal Barrier Resources Area zones.

CBRA prohibits the sale of NFIP flood insurance in CBRS units for structures built or substantially improved on or after October 1, 1983, or the subsequent date that a CBRA zone was identified. CBRA zones and their identification dates are shown on Flood Insurance Rate Maps (FIRMs).

You can determine whether your property is in a CBRA area on the Federal Emergency Management Agency (FEMA) website.

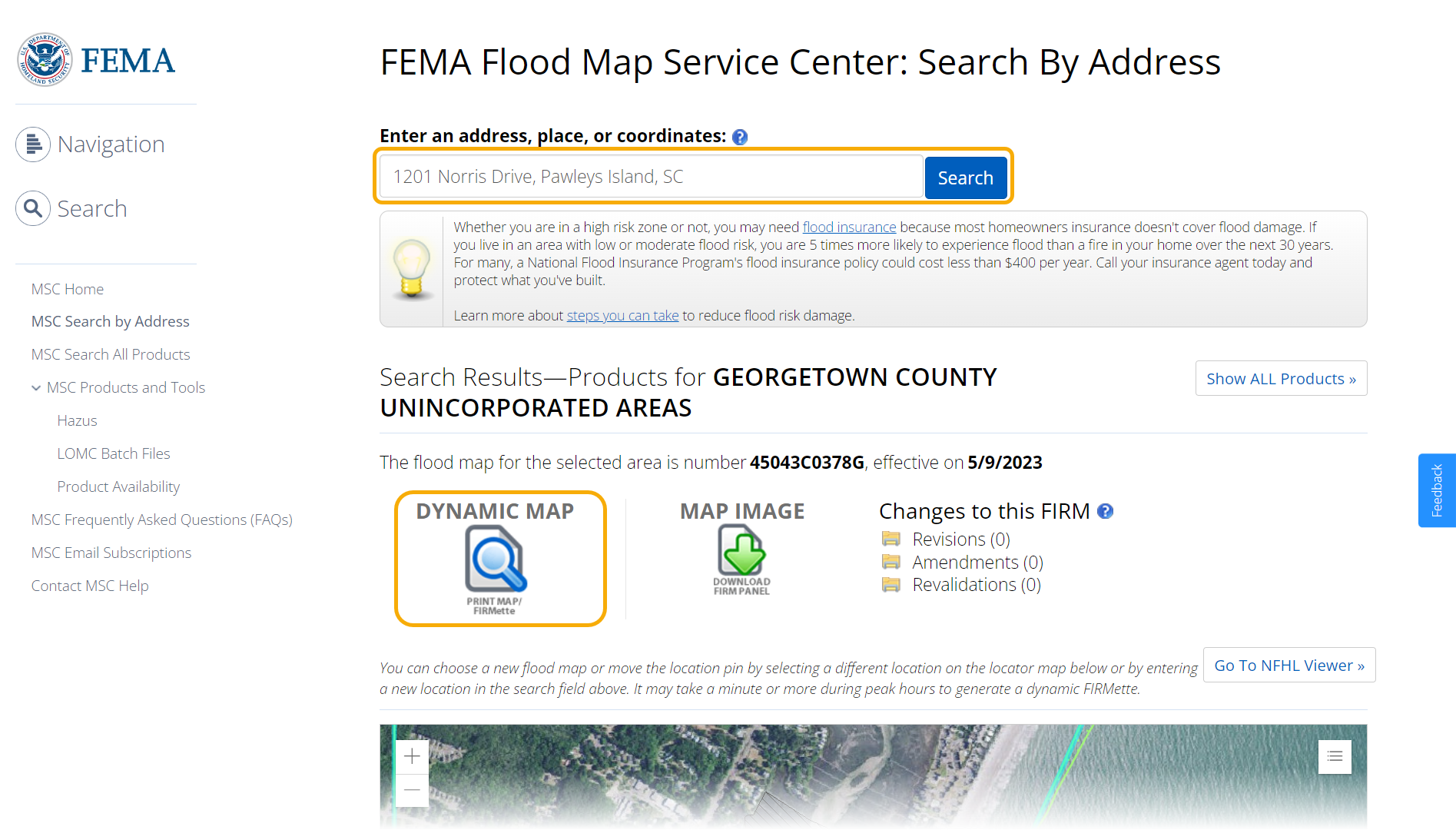

1. Go to msc.fema.gov/portal/search.

2. Enter the property's complete address and click Search. Once the search results appear, click the Dynamic Map option.

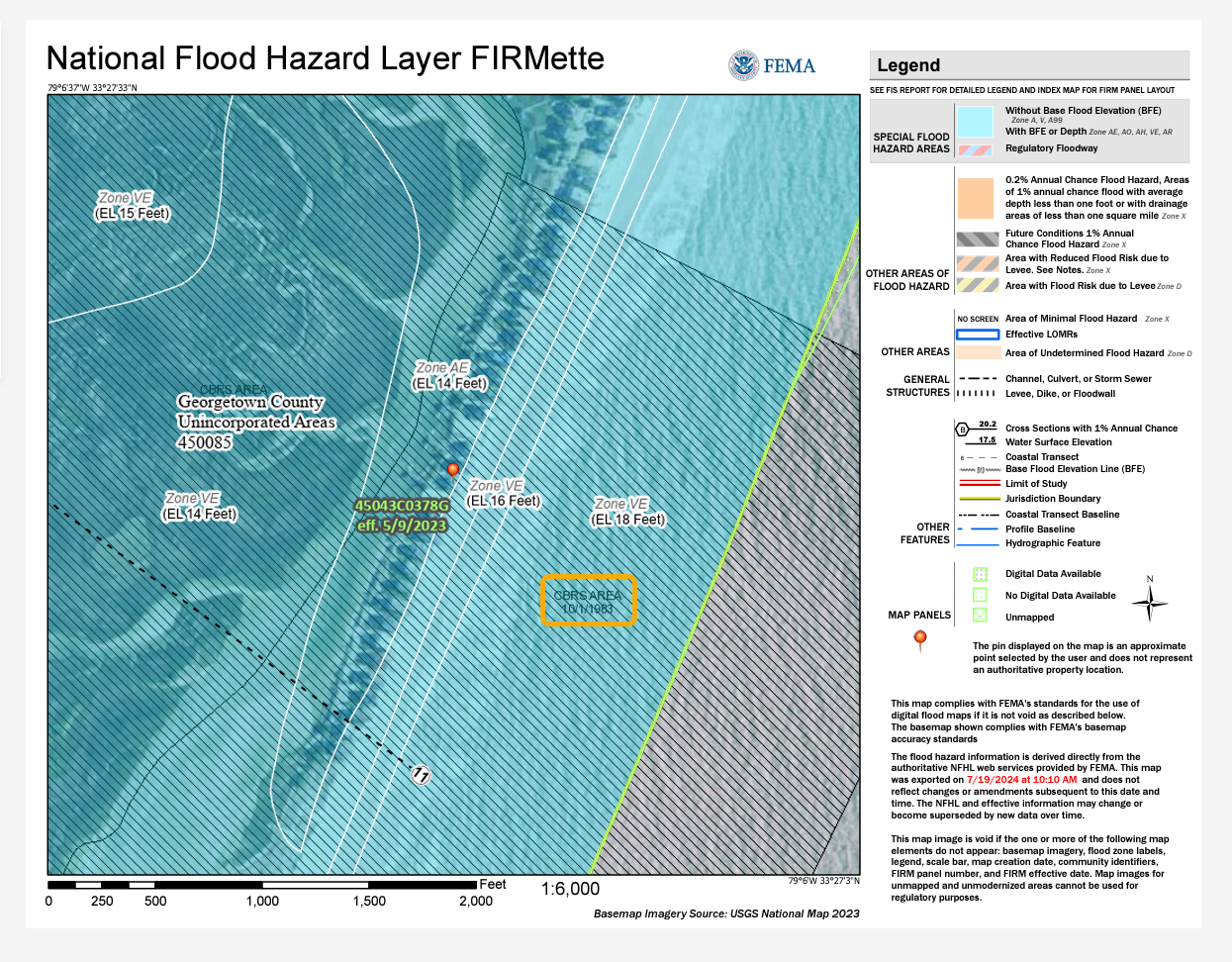

2. The process may take a few minutes. However, once the Dynamic Map is downloaded, you will see that for the \\\\\ hash, this represents the CBRA area as follows:

Flood zone

A flood zone is a defined geographic area with a specific flood hazard risk. They are indicated in a community's flood map.

You can determine your property's flood zone on the Federal Emergency Management Agency (FEMA) website.

1. Go to msc.fema.gov/portal/search.

2. Enter the property's complete address and click Search. Once the search results appear, click the Dynamic Map option.

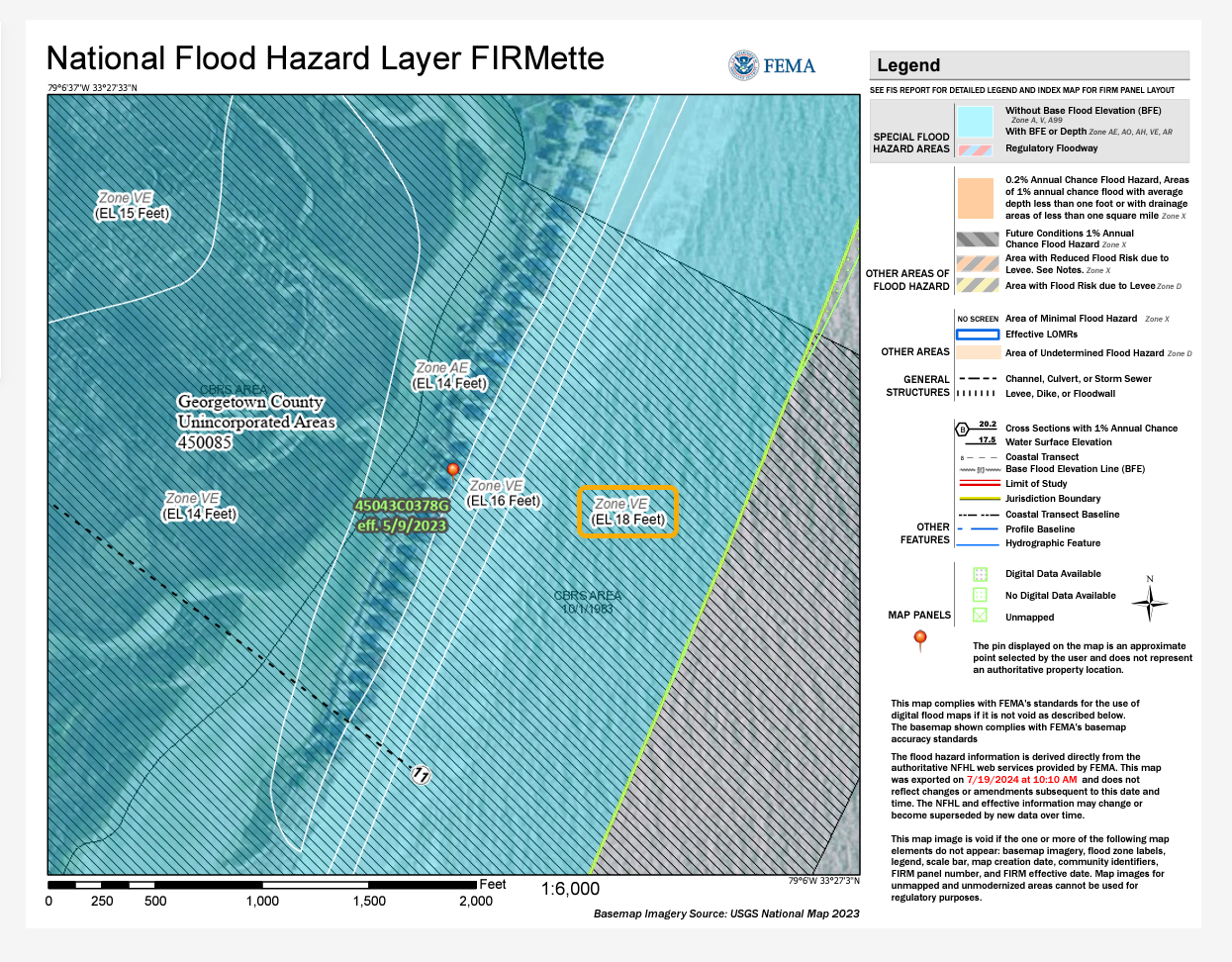

3. The Dynamic Map indicates flood zones as follows:

Non-Participating Community

The Community Rating System (CRS) is a voluntary incentive program that recognizes and encourages community floodplain management practices that exceed the minimum requirements of the National Flood Insurance Program (NFIP). Over 1,500 communities participate nationwide.

In CRS communities, flood insurance premium rates are discounted to reflect the reduced flood risk resulting from the community's efforts.

You can determine whether your property is in a Non-Participating Community on the Federal Emergency Management Agency (FEMA) website.

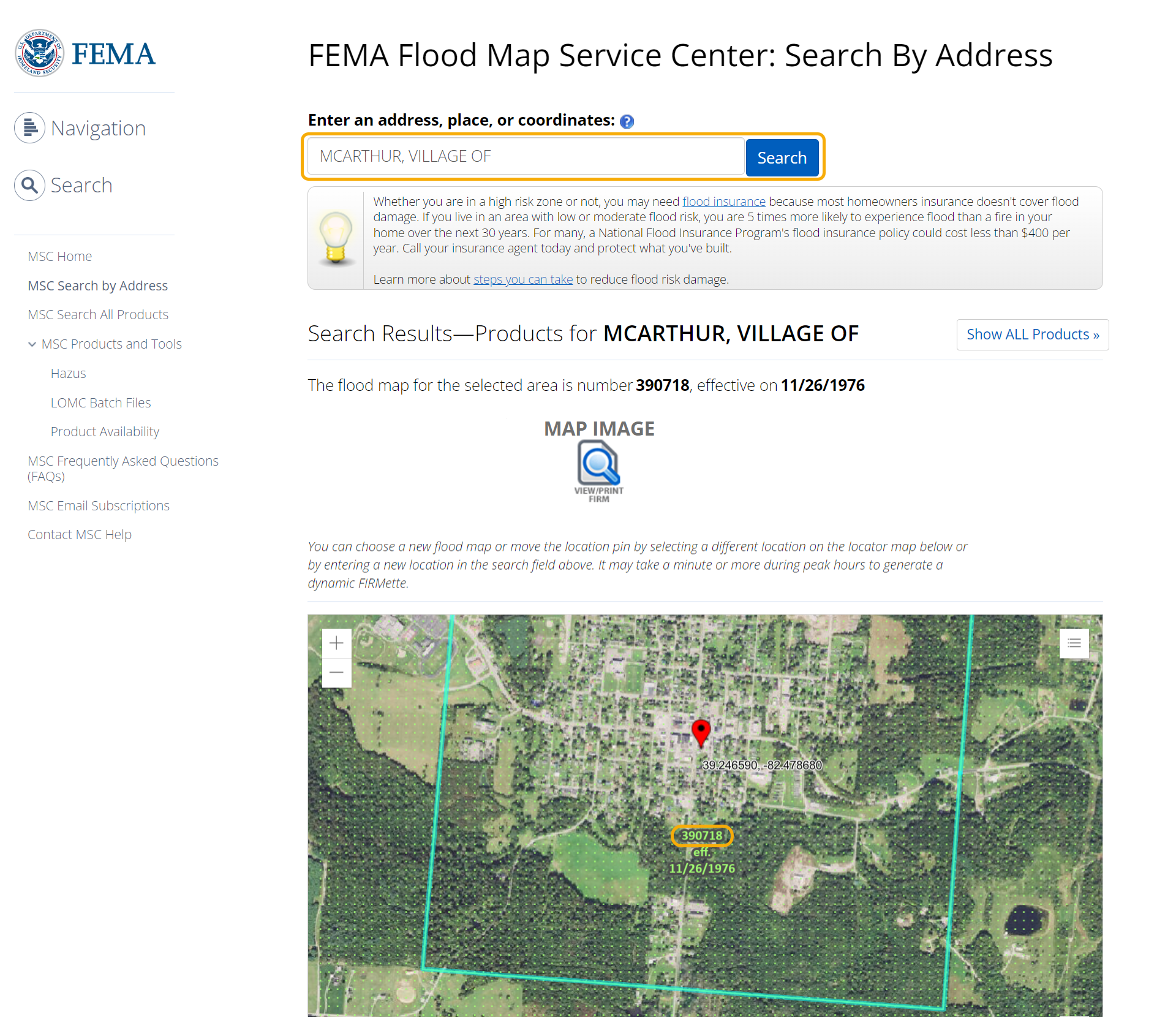

1. Go to msc.fema.gov/portal/search.

2. Enter the property's complete address and click Search. Once the search results appear, record the Community Number from the map. In this example, the Community Number is 390718.

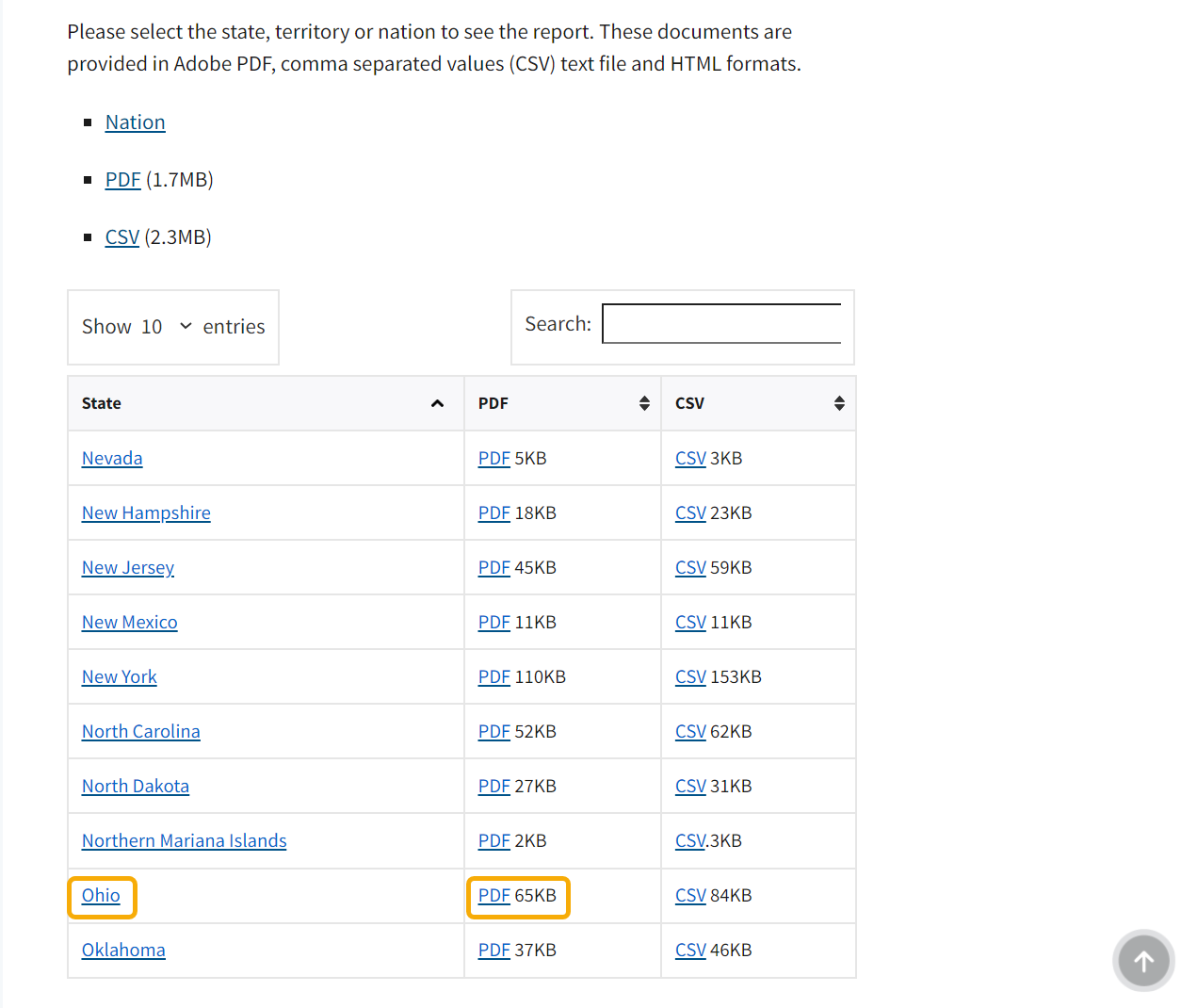

3. Once you know the Community Number, go to fema.gov/flood-insurance/work-with-nfip/community-status-book.

4. Scroll down the page to the individual States (the Find a Community Status Report section). Then, click the State the property is located in:

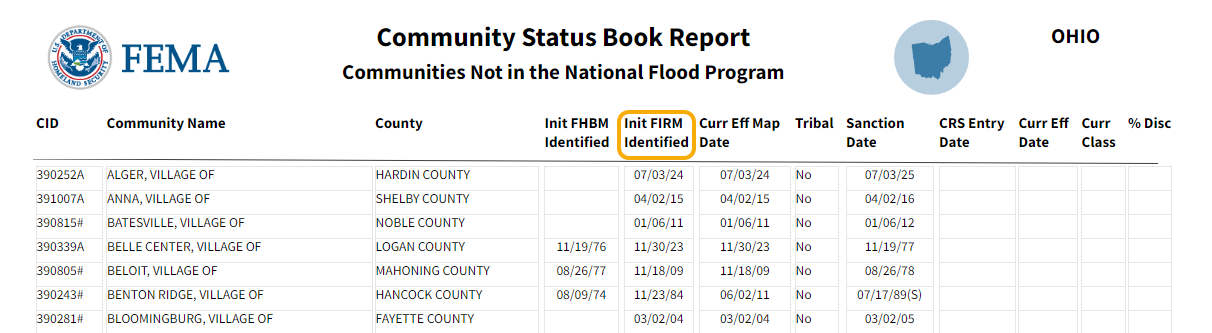

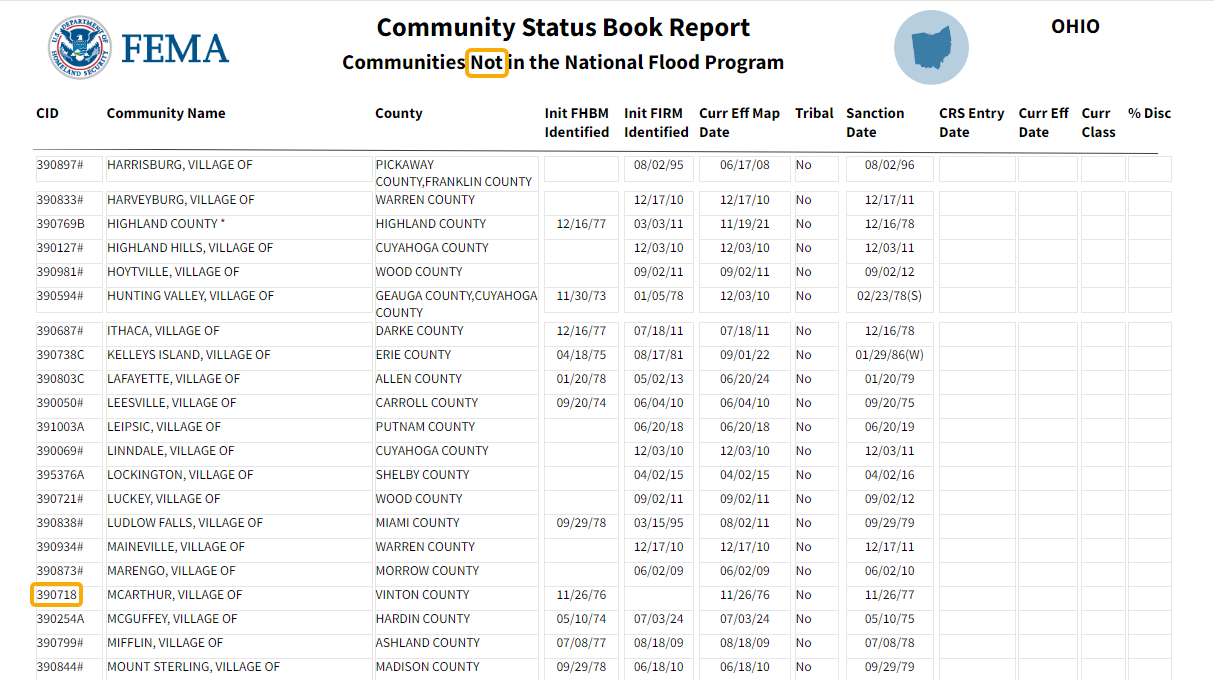

5. The list of Non-Participating Communities will appear on the last few pages of the Community Status Book Report of each State:

Suspended or Emergency Status

You can determine whether your property is located in a community that is currently in a Suspended or Emergency Status in FEMA's Community Status Book Report.

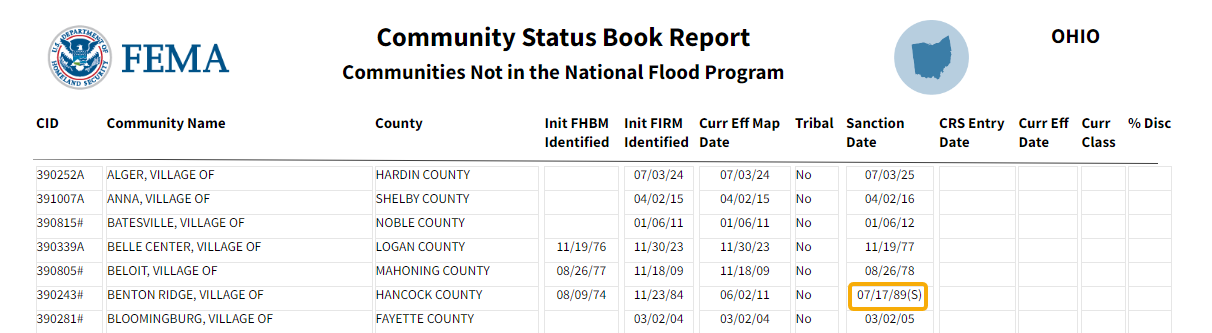

1. Open the Community Status Book Report for the State your property is located in. You can find the report as described above.

2. In the Community Status Book Report, communities in a Suspended or Emergency Status are indicated with the letter (S) or (E), respectively.

Pre or Post FIRM

Pre-Flood Insurance Rate Map (FIRM) buildings are buildings for which construction or substantial improvement occurred on or before December 31, 1974 or before the effective date of an initial Flood Insurance Rate Map (FIRM).

Pre-Flood Insurance Rate Map (FIRM) buildings are those built before the effective date of the first Flood Insurance Rate Map (FIRM) for a community.

This means they were built before detailed flood hazard data and flood elevations were provided to the community and usually before the community enacted comprehensive regulations on floodplain regulation.

Pre-FIRM buildings can be insured using "subsidized" rates. These rates are designed to help people afford flood insurance even though their buildings were not built with flood protection in mind.

You can determine whether your property is Pre- or Post-FIRM in FEMA's Community Status Book Report.

1. Open the Community Status Book Report for the State your property is located in. You can find the report as described above.

2. In the Community Status Book Report, find the effective date of the community's initial Flood Insurance Rate Map in the Init FIRM Identified column.

If your property was constructed before that, it's Pre-FIRM. If it was built after, it's Post-FIRM.